www.1percentblog.com

Saturday 17 March 2012

Friday 16 March 2012

Moving House

On the advice of a pal and before it gets too complicated to do, I shall be moving the blog over to a different host.

For the time being I have disconnected www.1percentblog.com from iam1percent.blogspot.com

In a few days I will migrate everything towards the new domain but until then, your favourite finance / miscellaneous blog will remain at it's blogspot address:

http://iam1percent.blogspot.com

For the time being I have disconnected www.1percentblog.com from iam1percent.blogspot.com

In a few days I will migrate everything towards the new domain but until then, your favourite finance / miscellaneous blog will remain at it's blogspot address:

http://iam1percent.blogspot.com

We Have Hit 1,000

After only 16 days of blogging the viewer mark has surpassed 1,000.

Thanks for everyone who has read and used our sponsors. Let's hope I don't get bored of writing in the near future

Thanks for everyone who has read and used our sponsors. Let's hope I don't get bored of writing in the near future

Today is my Last Day at the Church of England

Today

is my last day at the Church of England. After almost 12 years at the

firm — first as a summer intern at my local diocese, then in Wales for

10 years, and now in London — I believe

I have worked here long enough to understand the trajectory of Gods

culture, its people and its identity. And I can honestly say that my

’people’ are now is as toxic and destructive as I have ever seen it.

To

put the problem in the simplest terms, the interests of the church

continue to be sidelined in the way the people just want to have sex and

make some 'shekels'. God is one of the world’s

largest and most important beings and it is integral that people

continue to follow him for more than an insurance policy after death.

The people have veered so far from the message I preached right out of

pope college (Popelege for those ITK) that I can no

longer in good conscience say that I identify with what they think God

stands for.

It

might sound surprising to a skeptical public, but culture was always a

vital part of Christianities success. It revolved around teamwork,

integrity, a spirit of humility, and always

doing right by our fellow man, well apart from those Scientology nut

jobs. The culture was the holy water that made this place great and

allowed us to earn our followers trust for 2012 years. It wasn’t just

about the prayers; this alone will not sustain a

religion for so long. It had something to do with pride and belief in

the church. I am sad to say that I look around today and see virtually

no trace of the culture that made me love working for this God for so

many years. I no longer have the pride, or the

belief.

But

this was not always the case. For more than a decade I recruited and

mentored non believers through our grueling interview process. I was

selected as one of 10 bishops (out of a religion

of more than 30,000) to appear on our recruiting video, which is played

in every church we visit around the world. In 2006 I managed the summer

communion and the mixed sex lawn tennis cup.

I

knew it was time to leave when I realized I could no longer look

believers in the eye and tell them what a great saviour Jesus was.

When

the history books are written about Christianity, they may reflect that

the current chief executive officer, God, and the president, Jesus,

lost hold of the religion’s culture on

their watch. I truly believe that this decline in the people’s moral

fiber represents the single most serious threat to our long-run

survival.

Over

the course of my career I have had the privilege of advising the only

religion on the planet, five annual rallies in the United States, and

kept the piece with heathens in the Middle

East and Asia. If you had to put a number to it, my congregation has a

total belief base of more than a trillion dollars! I have always taken a

lot of pride in advising my congregation to do what I believe is right

for them, even if it means less money and

less co-mingling. This view is becoming increasingly unpopular in the

world. Another sign that it was time to leave.

What

are three quick ways to be a good human? a) ‘Get laid a lot’ which is

earth-speak for persuading the opposite sex to have sex with you, just

because it feels good (disgusting). b)

‘Get a sweet Ride’. In English: Spend less money in church and more at

work in order to get fancy cars than can’t even get around in London

anyway. c) Find yourself sitting in a seat where people around you

believe that religion can be all about sitting under

a bloody tree..

It

makes me ill how callously people talk about ripping their congregation

off. Over the last 12 months I have seen five different bishops refer

to their own congregation as “muppets,”

Even after Robert Finn, John Magee and Charles Brown? No humility? I

mean, come on. Integrity? It is eroding. I don’t know of any illegal

behavior, but will people push the collection tins and pitch lucrative

and complicated ways to gain enlightenment even

if they are not the simplest prayers or the ones most directly aligned

with the congregation’s goals? Absolutely. Every day, in fact.

These

days, the most common question I get from junior bishops about God is,

“If he is all loving, why is there such sorrow in the world?” It bothers

me every time I hear it, because

it is a clear reflection of what they are observing from their bishops

about the way they should behave.

When

I was a first-year bishop, I didn’t know where the bathroom was, or how

to tie my shoelaces. I was taught to be concerned with finding out what

the seven sacraments were, understanding

God, getting to know our congregation and what motivated them, learning

how they defined success and what we could do to help them get there.

My

proudest moments in life — steering clear of all that altar boy bunkem,

winning a bronze medal for the sack race in Vatican City, known as the

Papal Olympics — have all come through

hard work, with no shortcuts. Christianity today has become too much

about shortcuts and not enough about achievement. It just doesn’t feel

right to me anymore.

Bish’ Out

The century bond

After doing what I consider to be a decent job in managing the economy, Mr Osbourne has to go and put his foot in his mouth. He believes that it would be prudent to test the appetite for extremely long dated bonds with the use of the century bond. For those less versed in economics the bond will pay you a coupon of eg 4% of the value of the bond each year for 100 years, then give you back your initial money in the year 2112. This bond seems to have many similarities to the war bond in that it isn't inflation linked and carries a constant coupon for a long period of time.

I suppose I can vaguely understand why he would like to issue this bond. With a fragile economy, nervous investors and a looming downgrade of uk debt, it is a possibility that investors become spooked and sell their bond holdings. When the current bonds expire, investors may demand a greater coupon to justify their continued investment and so the cost to service uk debt would increase.

By financing part of our debt with these instruments, the govt won't need to worry about the near term as they are fully funded for an extremely long period of time.

On the face of it, This sounds fantastic but we are assuming that investors will buy it and there lies the problem

The investors who buy these bonds know all of the above and are unlikely to buy such a long dated bond when the risks to the economy are so great. In fact a failed auction may become a self fulfilling prophecy.

Furthermore these long dated bonds are much more sensitive to changes in interest rates and economic developments than shorter dated bonds (as changes will affect a longer stream of coupons) so these bonds would actually be more volatile for investors.

Finally ask an analyst to forecast 3 years out in advance. 50% of the time he is right.... How can you possibly model a 100 year bond ?

I believe that war bonds sold as they were something that was beyond an investment . To buy a war bond was to help your country defeat the Nazis, "Lend to Defend Your Right To Be Free" and "War Bonds are Cheaper Than Wooden Crosses" are a lot more catchy than "Buy an Osboune Bond.....cos Labour Fucked It"

I suppose I can vaguely understand why he would like to issue this bond. With a fragile economy, nervous investors and a looming downgrade of uk debt, it is a possibility that investors become spooked and sell their bond holdings. When the current bonds expire, investors may demand a greater coupon to justify their continued investment and so the cost to service uk debt would increase.

By financing part of our debt with these instruments, the govt won't need to worry about the near term as they are fully funded for an extremely long period of time.

On the face of it, This sounds fantastic but we are assuming that investors will buy it and there lies the problem

The investors who buy these bonds know all of the above and are unlikely to buy such a long dated bond when the risks to the economy are so great. In fact a failed auction may become a self fulfilling prophecy.

Furthermore these long dated bonds are much more sensitive to changes in interest rates and economic developments than shorter dated bonds (as changes will affect a longer stream of coupons) so these bonds would actually be more volatile for investors.

Finally ask an analyst to forecast 3 years out in advance. 50% of the time he is right.... How can you possibly model a 100 year bond ?

I believe that war bonds sold as they were something that was beyond an investment . To buy a war bond was to help your country defeat the Nazis, "Lend to Defend Your Right To Be Free" and "War Bonds are Cheaper Than Wooden Crosses" are a lot more catchy than "Buy an Osboune Bond.....cos Labour Fucked It"

Thursday 15 March 2012

Wednesday 14 March 2012

1percentblog.com

I've pulled out all the stops and invested my hard earned cash into a domain name. Hope this makes finding my blog a little easier for everybody!

Until then...

Until then...

The Incredible Human Mind

Ins't it anzmaig taht you can usndarentd tihs snenatce eevn tgouh msot of the wodrs are selpt wnorg. Ducth rcehesraers drivcsoerd taht as lnog as the frsit and lsat ltteers are in the creroct pclae yuor barin wlil tltrasnae the stnceane itno a mroe radealbe famort.

Tuesday 13 March 2012

Student Debt Time Bomb

The Washington Post recently warned of a potential debt time bomb in the form of student loans, which they say have skyrocket from $100bn to $800bn in 4 years! This figure represents more than the US consumer's total credit card debt!

With student fees increasing from £3,000 to £6,000 (£9,000 for some uni's), I thought it prudent to wonder if the UK has the same problem.

What you will be happy to hear is that our student debt pile is worth just £30bn ($48bn), not even close to our brothers across the pond. The more astute readers would immediately realise that two absolute numbers cannot be compared until we put them in context.

Against GDP, US student debt pile (SDP) stands at 5%, while the UK SDP is at 2.5%. If we look at the number of domestic students in each country, the UK has 1.2m while the US has 14.6m. Normalising for US Students, the UK would have $580bn of debt.

So far it seems that the UK do not have as big a debt burden than the US. However factoring in the average cost of university (£6k to £20k per annum for US and UK's £3k) we can see a different story entirely. If the average cost for US students is roughly 4x more than UK while the US has 10x as many students, we would expect the debt burden in the US to be 40x the UK's. This clearly is untrue as the ratio is roughly 20x. A possible reason for this may be that a lower percentage of US students tend to use the student debt facilities in the first place (the average UK debt of $15k is a lot more palatable than US's $90k student debt).

What does all this mean? The Washington Post continues by telling us the amount of bankruptcy proceedings resulting from student debt has risen 80% a year as parents undersign their children's student loan with their assets. They use the story of a war vet whose house is endanger of foreclosure as his daughter has not managed to find a permanent job since graduating.

*Courtesy of the Daily Telegraph

*Courtesy of the Daily Telegraph

The questions I want to ask in this article are somewhat different. Firstly do we even have a problem? and second, will the increase in tuition create a debt time bomb down the line?

Is the debt load a problem *Govt loans only*

At this point it is prudent to split US students into two groups. According to statistics, around 50% of college goers attend a university with charging £6k per year. These are lower attainment universities and I would assume the average household earnings is lower. Conversely 25% go to £20k per year premium universities such as Yale or Harvard. In this group I will again assume that the amount of college goers that use loans is rather limited and so I will ignore this group altogether.

So with that in mind, upon graduation, US students typically have $25k debt (£18k) compared to the UK's £14k (this has more than doubled over 10 years). This goes hand in hand with the fact that they are expected to earn more (£33k vs £25k). The final piece of the puzzle is the interest rates payable on these loans. I will leave savings rates out simply because this generation tends not to be accurately portrayed in these analyses.

For the Brits, the APR on your debt is 1.5% while americans have to accept 3.5% rates, so annual interest for your average UK student is £210 and £540 for his American compatriot (0.84% of Gross earnings vs 1.6% respectively.)

On the face of it, despite UK being the clear winner, it does not seem that America has it that bad. Well the problem that America has is not in the affordability of debt but rather the availability of solid graduate jobs. The FT puts youth unemployment in the USA at about 17% whereas for the UK it is 21% and so even if the interest rate fees are cheap, how can a student pay them when he has no job!

In my humble opinion, one of the problems with human beings is that we are myopic in nature, ie we tend to attach way too much weight to the short term and hold less regard for any longer term developments. It seems that we are just in the lows of the business cycle and while I agree this low is potential more aggressive than the 'average low', it is certainly possible for recovery to occur. With this in mind, I do not believe that the current state of youth unemployment will cause the ballooning student debt pile to be a problem. Furthermore as these are govt credit mechanisms, it is perfectly feasibly for interest rate charges to be halted if the situation were to become increasingly dire.

Unfortunately, those who were privately financed to go through university have a more uncertain outcome, as the financial institutions that distribute this debt have to maximize profit, rather than social welfare.

Will the Increase in Fees Cause a Problem Down the Road?

The increase in fees will move student tuition from c.£3k to c£6k (and in some cases £9k, but those who pay the 9k will be members of the elite and probably wouldn't take a student loan anyway). Using numbers from the above, we can assume debt will increase to £25k (significantly more than the US). or £375 interest per month, which is still easily affordable.

Concluding this adventure into student loans, I think that the size of them is of little concern. What is concerning is the drive towards higher education. 50% of UK children now enroll in higher education and the problem is that this causes a dangerously one sided economy (which has already happened) and expectations of an increase in living standards when anyone knows that as the supply (of skilled labour grows) while the number of jobs remains constant, the average wage will decrease. If this were to be the case, the current crop of graduates would see a falling marginal benefit to university education. If we don't want an even bigger problem in 10 years, subsidize industries to take on youngsters while encouraging more applied learning channels.

With student fees increasing from £3,000 to £6,000 (£9,000 for some uni's), I thought it prudent to wonder if the UK has the same problem.

What you will be happy to hear is that our student debt pile is worth just £30bn ($48bn), not even close to our brothers across the pond. The more astute readers would immediately realise that two absolute numbers cannot be compared until we put them in context.

Against GDP, US student debt pile (SDP) stands at 5%, while the UK SDP is at 2.5%. If we look at the number of domestic students in each country, the UK has 1.2m while the US has 14.6m. Normalising for US Students, the UK would have $580bn of debt.

So far it seems that the UK do not have as big a debt burden than the US. However factoring in the average cost of university (£6k to £20k per annum for US and UK's £3k) we can see a different story entirely. If the average cost for US students is roughly 4x more than UK while the US has 10x as many students, we would expect the debt burden in the US to be 40x the UK's. This clearly is untrue as the ratio is roughly 20x. A possible reason for this may be that a lower percentage of US students tend to use the student debt facilities in the first place (the average UK debt of $15k is a lot more palatable than US's $90k student debt).

What does all this mean? The Washington Post continues by telling us the amount of bankruptcy proceedings resulting from student debt has risen 80% a year as parents undersign their children's student loan with their assets. They use the story of a war vet whose house is endanger of foreclosure as his daughter has not managed to find a permanent job since graduating.

The questions I want to ask in this article are somewhat different. Firstly do we even have a problem? and second, will the increase in tuition create a debt time bomb down the line?

Is the debt load a problem *Govt loans only*

At this point it is prudent to split US students into two groups. According to statistics, around 50% of college goers attend a university with charging £6k per year. These are lower attainment universities and I would assume the average household earnings is lower. Conversely 25% go to £20k per year premium universities such as Yale or Harvard. In this group I will again assume that the amount of college goers that use loans is rather limited and so I will ignore this group altogether.

So with that in mind, upon graduation, US students typically have $25k debt (£18k) compared to the UK's £14k (this has more than doubled over 10 years). This goes hand in hand with the fact that they are expected to earn more (£33k vs £25k). The final piece of the puzzle is the interest rates payable on these loans. I will leave savings rates out simply because this generation tends not to be accurately portrayed in these analyses.

For the Brits, the APR on your debt is 1.5% while americans have to accept 3.5% rates, so annual interest for your average UK student is £210 and £540 for his American compatriot (0.84% of Gross earnings vs 1.6% respectively.)

On the face of it, despite UK being the clear winner, it does not seem that America has it that bad. Well the problem that America has is not in the affordability of debt but rather the availability of solid graduate jobs. The FT puts youth unemployment in the USA at about 17% whereas for the UK it is 21% and so even if the interest rate fees are cheap, how can a student pay them when he has no job!

The short sighted man

In my humble opinion, one of the problems with human beings is that we are myopic in nature, ie we tend to attach way too much weight to the short term and hold less regard for any longer term developments. It seems that we are just in the lows of the business cycle and while I agree this low is potential more aggressive than the 'average low', it is certainly possible for recovery to occur. With this in mind, I do not believe that the current state of youth unemployment will cause the ballooning student debt pile to be a problem. Furthermore as these are govt credit mechanisms, it is perfectly feasibly for interest rate charges to be halted if the situation were to become increasingly dire.

Unfortunately, those who were privately financed to go through university have a more uncertain outcome, as the financial institutions that distribute this debt have to maximize profit, rather than social welfare.

Will the Increase in Fees Cause a Problem Down the Road?

The increase in fees will move student tuition from c.£3k to c£6k (and in some cases £9k, but those who pay the 9k will be members of the elite and probably wouldn't take a student loan anyway). Using numbers from the above, we can assume debt will increase to £25k (significantly more than the US). or £375 interest per month, which is still easily affordable.

Concluding this adventure into student loans, I think that the size of them is of little concern. What is concerning is the drive towards higher education. 50% of UK children now enroll in higher education and the problem is that this causes a dangerously one sided economy (which has already happened) and expectations of an increase in living standards when anyone knows that as the supply (of skilled labour grows) while the number of jobs remains constant, the average wage will decrease. If this were to be the case, the current crop of graduates would see a falling marginal benefit to university education. If we don't want an even bigger problem in 10 years, subsidize industries to take on youngsters while encouraging more applied learning channels.

Monday 12 March 2012

The Right To Buy

Today Mr. Cameron launched a dual assault on the UK housing market. The right to buy scheme has been resurrected allowing council owners to buy their properties for up to £75,000 below market value, while the 'new buy' scheme has been supercharged allowing first time buyers to purchase new build properties worth up to £500,000 with just a 5% deposit!!!!!

The size of these offerings is also impressive as the government will allow 100,000 purchases under the 'new buy' scheme which (assuming 250k per house) is £25bn of housing stock!

Putting this in perspective, Barratt Developments (a leading UK housebuilder) has an inventory of £3bn of which half of that is undeveloped. Carrying on this theme, Persimmon have inventory of £2bn (£1.5bn undeveloped), Bellway has £1.2bn (£0.7bn of which is undeveloped), Taylor Wimpey has £2.6bn (£2bn undeveloped.).

Of the UK's biggest housebuilders, total new builds (both pipeline and completed) stand at c.£11bn, which isn't even half the government's firepower. Even including other housebuilders it is obvious that this is going to have a huge impact in the property market.

These projects will come as a welcome relief to housebuilders who have been hit by increasing mortgage costs (cheers Halifax!) and to Convervative MP's who feared the party wouldn't do enough to help the working class.

Now about the budget deficit....

Putting this in perspective, Barratt Developments (a leading UK housebuilder) has an inventory of £3bn of which half of that is undeveloped. Carrying on this theme, Persimmon have inventory of £2bn (£1.5bn undeveloped), Bellway has £1.2bn (£0.7bn of which is undeveloped), Taylor Wimpey has £2.6bn (£2bn undeveloped.).

Of the UK's biggest housebuilders, total new builds (both pipeline and completed) stand at c.£11bn, which isn't even half the government's firepower. Even including other housebuilders it is obvious that this is going to have a huge impact in the property market.

These projects will come as a welcome relief to housebuilders who have been hit by increasing mortgage costs (cheers Halifax!) and to Convervative MP's who feared the party wouldn't do enough to help the working class.

Now about the budget deficit....

Pay Day Loans: Helpful or Hurtful?

With the economic downturn in full swing and people struggling to get by it only takes a few hours of television watching to come across this guy...

Wonga (after a $3m investment) is already in profit and apparently only issues money to 20% of applicants, leading to an exceptionally low default rate (when it first became mainstream I had a bet with a friend that this firm would never be profitable. Shows what I know!).... Despite the lack of a physical presence that would allow local pay day loans to threaten non payers, Wonga has an OTT algorithm that assesses a persons creditworthiness and I guess the proof of the pudding is in the eating.

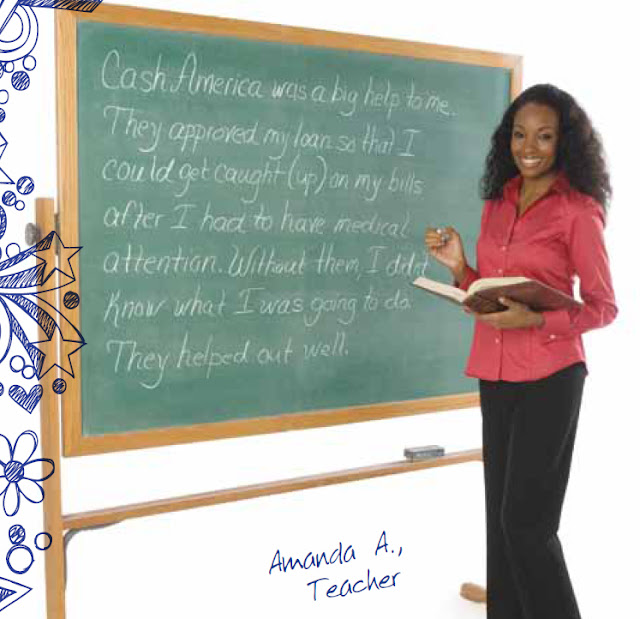

QuickQuid is another heavily advertised service which is actually an offshoot of a listed American money lender, Cash America. Over the past three years, revenues at this company have increased at light speed ($23m to $100m in 2 years of operation - net income on this level cannot be obtained).

It's nice to know that they are making money :s but is it simply a business that preys on the uninformed and the desperate?

1. With such eye popping APRs you could easily ask why these people don't extend finance on their houses, use an overdraft or even a credit card, all of which carries a much lower APR.

The proponents would argue that the APR rate is misleading. After al,l these payday loans are not meant for long periods of time and so a better way to look at it would be a £10 charge to settle a £100 bill. The APR is simply noted as part of regulation.

Why do people not take finance with either cheaper methods? Well for one, these financial needs are short term in nature and organising an extension of finance using more traditional channels may take up to two weeks. Furthermore, these people may not even have the credit rating required to use more traditional methods of finance and so how else are they going to pay a bill?

2. These companies promote financial irresponsibility by supercharging the buy now pay later crowd, whilst potentially opening customers up to a vicious debt spiral.

Once again the vendors would tell us that they make sure that they do their research on each customer and their stringent criteria refuses loans to those considered fiscally irresponsible. They could loan money to every schmoe in the country and their balance sheet would explode with accounts receivable. The problem is that many customers would't repay and then the vendors wouldn't have a business. It is therefore in the interests of both vendors and consumers that only more responsibile people use this service.

Unfortunately there will always be a few that keep rolling over debt and even realising the full APR - turning a £100 debt into a £5000 in a short space of time. Cash America tells us that they recognise when people have trouble paying and come to a mutual plan of repayment that may not include the full APR.

At first glance, I must say I was against the idea of pay day loans but thinking about it, as long as the country adds a degree of regulation to help those people who use them beyond the scope of the deal (as in rolling over month by month), I guess they do provide a niche service which is useful.

Banning Wonga from operation on the above grounds would be no different to banning casinos from operation. As we all (should) know, the house always wins in the long run. Therefore, gamble too much and you WILL lose money. Of course there are always a few that feel they can beat the system and spend their life savings on trying to do so (similar to those people who overuse pay day loans) but the highly regulated casino industry provides a lot of help for people that may have addictions as well as refusing them from gambling altogether.

Banning Wonga from operation on the above grounds would be no different to banning casinos from operation. As we all (should) know, the house always wins in the long run. Therefore, gamble too much and you WILL lose money. Of course there are always a few that feel they can beat the system and spend their life savings on trying to do so (similar to those people who overuse pay day loans) but the highly regulated casino industry provides a lot of help for people that may have addictions as well as refusing them from gambling altogether.

You will always get some people falling through the net, but unfortunately, as old Blue Eyes says, 'That's Life'

What do you think? Good do or Crap do?

*Earl from Wonga

He promises a fun and easy way to get a little bit of cash that you need when you have a bill due before your paycheck.

The cost? Well on Wonga's website, a 400GBP loan for 30 days costs £125 ! More realistially though, a £100 loan for 5 days costs only £10....

The cost? Well on Wonga's website, a 400GBP loan for 30 days costs £125 ! More realistially though, a £100 loan for 5 days costs only £10....

Below is a list of Wonga and it's rival's typical APR.

| Payday UK | 1737% |

| Quick Quid | 1734% |

| Wonga | 4214% |

| Payday Express | 1737% |

| Kwik Cash | 1737% |

| UK PaydayToday | 1737% |

Wonga (after a $3m investment) is already in profit and apparently only issues money to 20% of applicants, leading to an exceptionally low default rate (when it first became mainstream I had a bet with a friend that this firm would never be profitable. Shows what I know!).... Despite the lack of a physical presence that would allow local pay day loans to threaten non payers, Wonga has an OTT algorithm that assesses a persons creditworthiness and I guess the proof of the pudding is in the eating.

QuickQuid is another heavily advertised service which is actually an offshoot of a listed American money lender, Cash America. Over the past three years, revenues at this company have increased at light speed ($23m to $100m in 2 years of operation - net income on this level cannot be obtained).

*Cash America Annual Report 2010

It's nice to know that they are making money :s but is it simply a business that preys on the uninformed and the desperate?

1. With such eye popping APRs you could easily ask why these people don't extend finance on their houses, use an overdraft or even a credit card, all of which carries a much lower APR.

The proponents would argue that the APR rate is misleading. After al,l these payday loans are not meant for long periods of time and so a better way to look at it would be a £10 charge to settle a £100 bill. The APR is simply noted as part of regulation.

Why do people not take finance with either cheaper methods? Well for one, these financial needs are short term in nature and organising an extension of finance using more traditional channels may take up to two weeks. Furthermore, these people may not even have the credit rating required to use more traditional methods of finance and so how else are they going to pay a bill?

2. These companies promote financial irresponsibility by supercharging the buy now pay later crowd, whilst potentially opening customers up to a vicious debt spiral.

Once again the vendors would tell us that they make sure that they do their research on each customer and their stringent criteria refuses loans to those considered fiscally irresponsible. They could loan money to every schmoe in the country and their balance sheet would explode with accounts receivable. The problem is that many customers would't repay and then the vendors wouldn't have a business. It is therefore in the interests of both vendors and consumers that only more responsibile people use this service.

Unfortunately there will always be a few that keep rolling over debt and even realising the full APR - turning a £100 debt into a £5000 in a short space of time. Cash America tells us that they recognise when people have trouble paying and come to a mutual plan of repayment that may not include the full APR.

At first glance, I must say I was against the idea of pay day loans but thinking about it, as long as the country adds a degree of regulation to help those people who use them beyond the scope of the deal (as in rolling over month by month), I guess they do provide a niche service which is useful.

You will always get some people falling through the net, but unfortunately, as old Blue Eyes says, 'That's Life'

What do you think? Good do or Crap do?

Friday 9 March 2012

Alex Hope: Successful Trader or Marketing Ploy

As many of you no doubt have read, a 23 year old trader named Alex Hope walked into The Playground (a nightclub in Liverpool) and spent over £200,000 in a nightclub including one 30l bottle of Ace Of Spades Champagne. Story here.

His website http://www.alexhopefx.com/ was taken down but twitter profile @alexhopefx is still active

The media had a field day as yet another 'overpaid banker' enjoyed extravagance in the midst of recession. Many of us read in disbelief that a 23 year old could amass so much money by simply reading charts #voodooeconomics.

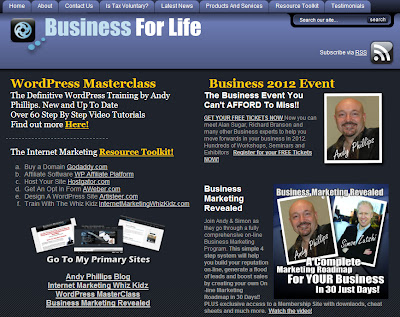

Using some rudimentary knowledge of website registration and advanced googling, I found out that his website, Alexhopefx.com is not even owned by Alex Hope, but by Andrew Philips of 'Business For Life LTD'. The domain itself only in existence for 5 months!

Maybe I am just jealous or just a little skeptical but I believe that this story may have an alterior motive. I cannot believe that: first, a person can amass so much money by purely reading charts. Second, I do not believe that someone with such success on the stock market would celebrate in such an OTT way. Third, traders don't do 'business deals'. Fourth, for £200,000 he could have chartered a jet and flown with 30 of his mates to Vegas for a full week of carnage whilst saving enough money for a luxury car. Fifth, with all the media attention and the mass ownership of camera phones, I am a little astounded that no pictures have appeared linking this guy and the 30l bottle together.

I don't doubt that Alex Hope trades (his twitter has 5k posts which would take a lot of time to conjure up) but I think that he has taken part in this story with the view to enhance his reputation as a trader and maybe gain a few quid selling his story or increasing attendance figures at any trading seminar he decides to run. Charging 200 people for a seminar is a much easier and safer way than punting on currencies with the sole help of charting!

So that's my view, in the meantime I will Tweet up Andy Phillips to see what he has to say on this brilliant story

His website http://www.alexhopefx.com/ was taken down but twitter profile @alexhopefx is still active

The media had a field day as yet another 'overpaid banker' enjoyed extravagance in the midst of recession. Many of us read in disbelief that a 23 year old could amass so much money by simply reading charts #voodooeconomics.

Using some rudimentary knowledge of website registration and advanced googling, I found out that his website, Alexhopefx.com is not even owned by Alex Hope, but by Andrew Philips of 'Business For Life LTD'. The domain itself only in existence for 5 months!

"But who is Andrew Phillips" I hear you say... According to his twitter @andyphillips101 he is an internet marketing and social media specialist.

The plot thickens! This Alex Hope story seems to have got the whole country talking about Playground Liverpool and as the recession is biting much more significantly in Liverpool, it seems that national interest for the price of £30k (rough cost price of the alcohol - even if it was all drunk; even if it was all even opened) is a good deal!

I don't doubt that Alex Hope trades (his twitter has 5k posts which would take a lot of time to conjure up) but I think that he has taken part in this story with the view to enhance his reputation as a trader and maybe gain a few quid selling his story or increasing attendance figures at any trading seminar he decides to run. Charging 200 people for a seminar is a much easier and safer way than punting on currencies with the sole help of charting!

So that's my view, in the meantime I will Tweet up Andy Phillips to see what he has to say on this brilliant story

Why do we Care About Whisper Numbers

We've all seen it, non farms out in a few hours and suddenly emails and bloombergs begin streaming in from mates, brokers and newswires. The number is next squawked round the trading room and everyone gets visibly more excited......

...Then the suckers come in and begin buying or selling futures in the direction of the surprise. If the whisper is higher than expected (more peeps on the payroll), the market begins to rise and vice versa. For the next two hours these guys and girls start deciding what they are going to do with all the money they make from their low risk, high return trade.....

50% of the time, they make money and what a whisper number! How intelligent are we?... The other 50% of the time 'Well it was only a whisper any way'..

I love how thousands of supposedly clever people even bother wasting their breath on this number when if they thought about it, THERE IS NO POSSIBLE WAY THAT THE WHISPER NUMBER HAS ANYTHING TO DO WITH WHAT'S ABOUT TO BE RELEASED!!!

Think about it. Reporters are gathered in a room, security checked and without mobile phones. They are then given a laptop with no internet connection and then, (all under tight security) given the number 30 mins early. This allows them to write their report to publish when the number is released to the general public.

All a whisper number is an estimate from a piece of macro research (and bear in mind that this number is one of the many numbers that make up the consensus) whose message is slowly convoluted from one guy sending another girl an interesting piece of research to, 'guys I have the number and boy are you gonna make money from trading it'...

..Don't me a favour, if a whisper comes today, have a dairy milk instead.*^

*For all US readers, sorry it doesn't make sense

^For all UK readers, sorry for the terrible joke.

...Then the suckers come in and begin buying or selling futures in the direction of the surprise. If the whisper is higher than expected (more peeps on the payroll), the market begins to rise and vice versa. For the next two hours these guys and girls start deciding what they are going to do with all the money they make from their low risk, high return trade.....

50% of the time, they make money and what a whisper number! How intelligent are we?... The other 50% of the time 'Well it was only a whisper any way'..

I love how thousands of supposedly clever people even bother wasting their breath on this number when if they thought about it, THERE IS NO POSSIBLE WAY THAT THE WHISPER NUMBER HAS ANYTHING TO DO WITH WHAT'S ABOUT TO BE RELEASED!!!

Think about it. Reporters are gathered in a room, security checked and without mobile phones. They are then given a laptop with no internet connection and then, (all under tight security) given the number 30 mins early. This allows them to write their report to publish when the number is released to the general public.

All a whisper number is an estimate from a piece of macro research (and bear in mind that this number is one of the many numbers that make up the consensus) whose message is slowly convoluted from one guy sending another girl an interesting piece of research to, 'guys I have the number and boy are you gonna make money from trading it'...

..Don't me a favour, if a whisper comes today, have a dairy milk instead.*^

*For all US readers, sorry it doesn't make sense

^For all UK readers, sorry for the terrible joke.

Thursday 8 March 2012

Sterilized QE: What is it?

Its impact the market barely registering as FED's highly accomodative monetary policy (that's low rates and QE) was given a hint of its future courtesy of the wall street journal.

*GBPUSD

*GBPUSD

Hilsenrath (of the WSF) told us that the FED were considering steriliz(s)ed QE as the US continue to engineer their way out of recession. Just one question on everyone's minds, just what is sterilized QE?

Sterilization in its usual sense refers to the used of foreign exchange (buying or selling your currency) in order to neutralise the effect that your operation has on the money supply of your currency. In this case it is ever so slightly different.

As I understand it (and I could be way off the mark!)...

1. FED prints money...

2. Fed then purchases bonds and other securities (speculation of Mortgage backed ones)

3. Fed now have bonds and money managers have loads of cash on their balance sheet, which they have until now simply re-deposited back into the FED (so much so that the yield is negative - ie saving could lose you money).

4. Bernanke doesn't want the money to remain idle and so simultaneously borrows the money that he has just paid the money managers for a small amount of interest.

5. As well as having more assets on the balance sheet (re bonds), they also now have liabilities (interest to be paid on the borrowing of money).

So in a nut shell money managers swap their bonds for a loan. As opposed to a lump sum, they get interest payments making it less convenient to deposit in a bank.

Why the change in tact?? Some commentators say it is to alleviate fears of inflation down the road. As the Weimar Republic showed us, inflation came only 5 years after the printing presses were turned on and once it reared its ugly head, well

Hilsenrath (of the WSF) told us that the FED were considering steriliz(s)ed QE as the US continue to engineer their way out of recession. Just one question on everyone's minds, just what is sterilized QE?

Sterilization in its usual sense refers to the used of foreign exchange (buying or selling your currency) in order to neutralise the effect that your operation has on the money supply of your currency. In this case it is ever so slightly different.

As I understand it (and I could be way off the mark!)...

1. FED prints money...

2. Fed then purchases bonds and other securities (speculation of Mortgage backed ones)

3. Fed now have bonds and money managers have loads of cash on their balance sheet, which they have until now simply re-deposited back into the FED (so much so that the yield is negative - ie saving could lose you money).

4. Bernanke doesn't want the money to remain idle and so simultaneously borrows the money that he has just paid the money managers for a small amount of interest.

5. As well as having more assets on the balance sheet (re bonds), they also now have liabilities (interest to be paid on the borrowing of money).

So in a nut shell money managers swap their bonds for a loan. As opposed to a lump sum, they get interest payments making it less convenient to deposit in a bank.

Why the change in tact?? Some commentators say it is to alleviate fears of inflation down the road. As the Weimar Republic showed us, inflation came only 5 years after the printing presses were turned on and once it reared its ugly head, well

Is this guy looking for an understudy?

Personally I am less inclined to think that the FED's operations thus far are inflationary...... The money created has

1. Hoarded with banks and institutions and has not joined the monetary in circulation (this could well change in the future).

2. The crisis was caused by rampant credit creation and so as credit is reduced, the money supply is reduced. In order to increase money supply, new money must exceed the contraction in credit.

Trying to get back on topic I hope the post explained what sterilized QE means. As for what it will do to the economy, your guess is as good as mine!

Wednesday 7 March 2012

The Greeks, The Bonds and The Hedgies

He looks confident, the stark warning he issued to Gomez and his crew has already forced a few of them to switch sides. 40% he thinks, but because Harry forgot his contact lenses, he can't give a precise estimate.

The watching crowd are undecided....

Only yesterday the crowd thought that Gomez Sachs and his possee would back down (hence the crowd trading at 25c on the Eur, or a reduction of 75% after PSI acceptance), but a glimmer of hope has spread among them.

If Gomez and his crew can hold out until March the 24th, Gomez would win one of the best duels he has ever come across. They give up and Harry the Greek throws us worthless bonds and the possee lose 8c on the dollar, we remain strong and we make 66c on the dollar!

Moving away from my Western themed arguement, what are the possibilities by 9pm??

1. Well, PSI take up could exceed 66% and CaC's are enforced on the stragglers. One would have thought CDS would then be activated and volatility aside, Greece will lower it's burden.

2. Maybe PSI would exceed 95%! No questions asked, Greece lowers its burden.

3. It hasn't got 66%, it will cheekily extend the deadline and maybe throw a few sweeteners in.

4. The hedgies hold out and leave the PSI voting panel after March the 24th, with 100c on the Euro courtesy of the ECB.

5. The hedgies hold out and declare a default, panic ensues....Who's next ??

What do you think partner? Are those 33c bonds looking to good to pass up, or did you buy them yesterday for 25c and taken on what is essentially a free option.

It's Not Greece We Should Worry About, It's CHINA!

Tin hats to the ready chaps! Yesterday saw a remarkable rout in world equity markets. The reason? Greek ministry of finance issued a thinly veiled warning telling all you bondholder scumbags to accept the 75% NPV reduction in your bonds or else we will default and watch contagio sweep across your portfolio's muahahahaha.

However, in a country but only a few hours flight away, the Mr President Wen told us that China was targetting a 7.5% growth rate compared to c8.5% the year before (and one of the lowest in recent memory). Furthermore, they would now rebalance the economy from investment to consumption...

As the old adage goes, a picture paints a thousand words, so with the help of my trusty excel...

Armed with this knowledge, what would we expect to happen with China's demand for the above commodities and what would we expect this to do for their prices? Take a look at the nickel and Aluminium price charts...

The above lead me to conclude that a fundamental change in our economic landscape is about to occur. China who have been a relatively small importer of european and us products (c12% for European), may begin to import a lot more so I would pay particular attention to cars (Roads per car ratio @ 80x is the highest in the world, Spain at number two manages half that) and luxury consumer goods while cement producers (China uses 5x the annual average cement, or1,500kg per person per year) may well suffer!

Top down, I would have thought that there would be a lot of downard pressure on equity mkts in general as the worlds last burgeoning economy admits that the future isn't as bright.

Looking at Greece it is important to remember that only 75bn Eur of debt still remains on balance sheets, and even though the size and scope of contagion is completely uncertain the reduction in the Chinese GDP target represents a 35bn Eur decrease from the world economy.

RedRut, over and out...

Tuesday 6 March 2012

Paying For Other Peoples Mistakes

So the guys who own the mets and a substantial chunk of profit from Mr. Madoff are locking horns with the Madoff trustee to decide how much money they give back in order to repay others who were less fortunate in the whole debacle. So far $80m has to be paid with another $220m if they are found guilty of turning a blind eye to the suspicions of a ponzi scheme.

I have been in two minds since reading this little piece of news as I am sure many of you are. Why should they give any money back??? Fair enough the company was involved in a ponzi scheme but as far as the investors are concerned, how are they supposed to know? Surely if the court alleges they ignored obvious warning signs, they should be imprisoned for 5 years and given an unlimited fine (POCA).

On the other hand, as the hedge fund industry isn't well regulated, are they indirectly funding criminal activity? And if that is the case, we move into yet another facet of law....

How about another thought for the road, how have they determined how much they are supposed to give back in the first place? It's not like you can redistribute all profits and end up with every investor flat on inception. After the costs associated with running the business, someone is still going to lose out, and you can be damn sure that these legal beavers aren't working for free.

I have been in two minds since reading this little piece of news as I am sure many of you are. Why should they give any money back??? Fair enough the company was involved in a ponzi scheme but as far as the investors are concerned, how are they supposed to know? Surely if the court alleges they ignored obvious warning signs, they should be imprisoned for 5 years and given an unlimited fine (POCA).

On the other hand, as the hedge fund industry isn't well regulated, are they indirectly funding criminal activity? And if that is the case, we move into yet another facet of law....

How about another thought for the road, how have they determined how much they are supposed to give back in the first place? It's not like you can redistribute all profits and end up with every investor flat on inception. After the costs associated with running the business, someone is still going to lose out, and you can be damn sure that these legal beavers aren't working for free.

Monday 5 March 2012

Bretton Woods - Egyptian Style

I think everyone is more than familiar with the turmoil surrounding Egypt - after almost imploding into civil war, the population removed Preisdent Mubarak to make way for what they hope will be a fairer and more democratic society. Only time will tell if their wishes are fulfilled but in the meantime, let's turn to their currency, the Egyptian Pound.

I have graphed it against the USD and the GBP (I have left out the Euro for obvious reasons).....

I have graphed it against the USD and the GBP (I have left out the Euro for obvious reasons).....

Granted there has been a little bit of devaluation on the EGP's part but for a country that is going through the turmoil that it is, shouldn't the currency have been more aggresively sold?

Please turn your attention to the balance sheet of the Egyptian Central Bank where the following figures really stand out...

From March 11 to Jan 12 **Figures are in EGP mn

Net Foreign Assets reduced from 167,000 to 86,205 (Half of all foreign assets sold in 3/4 of a year!)

Net Domestic Assets increased from 67,454 to 174,414

Reserve Money (M0) increased slightly from 235,000 to 260,000

Circulation outside the Central bank increasing 40,000

This strikes me as a classic example of selling out all your foreign assets in order to keep your currency from devaluating and making foreign imports (most of the goods consumed in Egypt would be) more expensive. The only problem is, that the status quo can only be held for another 6 - 9 months (asssuming no speculative attacks on the currency).

Friday 2 March 2012

Do The Greeks Have a Choice?

Everybody's favourite European country has an agonising choice. It isn't anything new as you read about everyday in newspapers ranging from the FT to the Daily Star.....Either Greece accepts the harsh tonic that the ECB demand or they renege on their debt and leave the Eurozone altogether and take on the Drachma.

Of course there are sound arguments for both. Staying in the Eurozone guarantees them access to capital markets that (let's be honest) are sorely needed. Defaulting on the debt would antagonize its trading allies and the financial institutions that buy the debt in good faith. Plus if you are already running a budget deficit and need to plug holes in your leaky economy, you are going to have to print money and we all know where that leads right Weimar Republicans? (aka inflation)

If they did default, would it be that bad? The drachma would surely be devalued giving them a greater competitive advantage and a chance to kick-start their economy (primarily their tourism economy), while the Central bank gain autonomy over their monetary policy, allowing them to further fine tune the economy....

Problem is that we all assume that the currency would be freely tradable; that you can go to a Travelex and change your $/£/Eurs for Drachma but who in their right mind would agree (even at favourable rates) to take stock of a currency that is so volatile you could lose 5 - 10% of your money in a week. Furthermore, if hyperinflation takes hold the situation would be even worse.

So there you go, the populous is forced to trade in drachmas but when the Greek grocery store wants to stock up on M and M's, how is it going to pay Nestle for the sweets? It can't convert its drachma's into anything other currency so it can't have any M and M's.....

Fair enough, there will always be someone that would take the risk at the right price but taking on the drachma could well mean the end of foreign supply of goods, at least in the near term.

Greece with no M and Ms? I sure hope not

Of course there are sound arguments for both. Staying in the Eurozone guarantees them access to capital markets that (let's be honest) are sorely needed. Defaulting on the debt would antagonize its trading allies and the financial institutions that buy the debt in good faith. Plus if you are already running a budget deficit and need to plug holes in your leaky economy, you are going to have to print money and we all know where that leads right Weimar Republicans? (aka inflation)

If they did default, would it be that bad? The drachma would surely be devalued giving them a greater competitive advantage and a chance to kick-start their economy (primarily their tourism economy), while the Central bank gain autonomy over their monetary policy, allowing them to further fine tune the economy....

Problem is that we all assume that the currency would be freely tradable; that you can go to a Travelex and change your $/£/Eurs for Drachma but who in their right mind would agree (even at favourable rates) to take stock of a currency that is so volatile you could lose 5 - 10% of your money in a week. Furthermore, if hyperinflation takes hold the situation would be even worse.

So there you go, the populous is forced to trade in drachmas but when the Greek grocery store wants to stock up on M and M's, how is it going to pay Nestle for the sweets? It can't convert its drachma's into anything other currency so it can't have any M and M's.....

Fair enough, there will always be someone that would take the risk at the right price but taking on the drachma could well mean the end of foreign supply of goods, at least in the near term.

Greece with no M and Ms? I sure hope not

Thursday 1 March 2012

A Free Lunch?

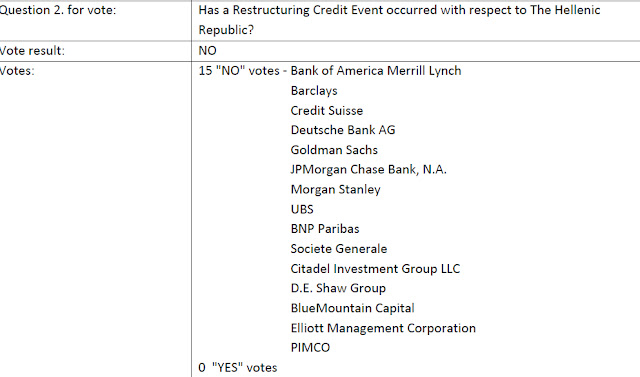

Today ISDA, those crazy kids decided that the bond swap for Greek debt did not constitute a credit event.

For those who don't know, ISDA are the group that determine whether or not your complex CDS (Credit Default Swap) will pay out or not. The theory goes that if the CDS underlying changes the terms of credit and because there are hundreds if not thousands of ways this could happen, you need a bunch of mavens (clever people) to tell you whether this consitutes a 'credit event'.

If you believe that the company/sovereign you have bought CDS against has committed a credit event and they disagree, you're not getting any cash......

You would think therefore, that ISDA are a group of mavens much like Standard and Poors in that they are independent and therefore don't lose or gain by the outcome of their decision.......Think again

Seems a little odd to me that the people who write these CDS are the same people that judge whether they are be fulfilled??

I don't know, maybe I am being a little harsh as theoretically a credit event has not yet occurred (no-one has yet been forced to accept a change in agreements they do not want) but one thnigs for sure, you are like to find less people that think CDS' are a great way to insure against default within your portfolio

For those who don't know, ISDA are the group that determine whether or not your complex CDS (Credit Default Swap) will pay out or not. The theory goes that if the CDS underlying changes the terms of credit and because there are hundreds if not thousands of ways this could happen, you need a bunch of mavens (clever people) to tell you whether this consitutes a 'credit event'.

If you believe that the company/sovereign you have bought CDS against has committed a credit event and they disagree, you're not getting any cash......

You would think therefore, that ISDA are a group of mavens much like Standard and Poors in that they are independent and therefore don't lose or gain by the outcome of their decision.......Think again

Seems a little odd to me that the people who write these CDS are the same people that judge whether they are be fulfilled??

I don't know, maybe I am being a little harsh as theoretically a credit event has not yet occurred (no-one has yet been forced to accept a change in agreements they do not want) but one thnigs for sure, you are like to find less people that think CDS' are a great way to insure against default within your portfolio

Welcome to the 1 Percent

Welcome to the 1 percent, where I and possibly a few other interesting individuals will be posting ramblings and musings on what is happening the world of finance.

With that goal in mind I guess it is pretty easy to figure out how I came across the name for this blog. In an age where my profession stands as the 'most hated profession in the world', it is rare that I can read a whole newspaper without an article relating to how the 99% (as they attractively call themselves) believe we are responsible solely for the economic pile of horse turd we currently find ourselves in....anyway bad blood aside, I thought that in being labelled indirectly as the 1%, I may as well get some use of it!

Who am I? Well I am a financial (semi) professional spending time at two investment banks while more recently plying my trade in a boutique derivatives house. Unfortunately, I don't want to open myself up to anything libelous so lets just play it safe and keep everything on an anonymous basis.....

I intend to set up a mailbox in the near future but until then, contact through the forum will be your only voice!!!

With that goal in mind I guess it is pretty easy to figure out how I came across the name for this blog. In an age where my profession stands as the 'most hated profession in the world', it is rare that I can read a whole newspaper without an article relating to how the 99% (as they attractively call themselves) believe we are responsible solely for the economic pile of horse turd we currently find ourselves in....anyway bad blood aside, I thought that in being labelled indirectly as the 1%, I may as well get some use of it!

Who am I? Well I am a financial (semi) professional spending time at two investment banks while more recently plying my trade in a boutique derivatives house. Unfortunately, I don't want to open myself up to anything libelous so lets just play it safe and keep everything on an anonymous basis.....

I intend to set up a mailbox in the near future but until then, contact through the forum will be your only voice!!!

Subscribe to:

Posts (Atom)